Startup Booted Fundraising Strategy

Table of Contents

ToggleNearly 90% of startups that approach investors too early are rejected, not because their idea is wrong, but because they show up before they have traction worth funding, according to the Kauffman Foundation’s 2025 Startup Funding Report. If you have been burning months chasing term sheets with nothing but a pitch deck, there is a smarter path forward in 2026. A well-executed startup booted fundraising strategy lets you build genuine leverage before you ever walk into a room with a VC.

As a Startup Growth Strategist and Founding Partner at ZProStudio, I have worked with over 60 early-stage founders across SaaS, fintech, and consumer brands. The ones who raised successfully almost always followed the same counterintuitive playbook: bootstrap first, raise on proof. This guide walks you through that entire framework, updated for the market realities of 2026.

What is a startup booted fundraising strategy?

A startup booted fundraising strategy is a capital-raising approach where founders first self-fund operations to achieve proof-of-concept, then leverage that traction to attract investors on far better terms. It works by combining disciplined bootstrapped startup fundraising with milestone-based investor outreach. Unlike seeking funding from day one, this method positions founders as low-risk, high-conviction operators, making it the preferred approach for 86% of seed investors surveyed by TechCrunch in 2025.

Why the Fundraising Game Changed Completely in 2025–2026

If you tried raising a pre-revenue seed round in 2023, you may have gotten away with it. In 2026, that window is effectively closed. The self-funded startup growth mindset is no longer just a frugal founder’s preference; it is what the market demands. According to PitchBook’s 2025 Venture Monitor, median seed-round valuations fell 22% year-over-year, while investor diligence timelines extended from an average of 6 weeks to 14 weeks. Investors have more leverage, and pre-traction founders have less.

Three forces converged to reshape early-stage fundraising as of early 2026. First, the post-2022 correction forced VCs to prioritize capital efficiency over growth-at-all-costs. Second, AI tools dramatically lowered the cost to build an MVP, eliminating the “I need funding to build” argument. Third, revenue-based financing and rolling funds made bootstrapped startup fundraising a genuine bridge to institutional capital rather than a consolation prize.

In my experience advising founders at ZProStudio, those who arrive at investor meetings with even three to six months of organic revenue data close rounds 40% faster and give up 15 to 20% less equity. The startup booted fundraising strategy is not about avoiding investors; it is about timing the relationship correctly.

Expert Insight: “Founders who bootstrap to their first $10K MRR before fundraising almost always negotiate from a position of strength. They know their unit economics, their customer acquisition cost, and their retention curve. That data is worth more than any pitch deck.” – Reid Hoffman, co-founder of LinkedIn, from his 2025 Masters of Scale interview on founder leverage.

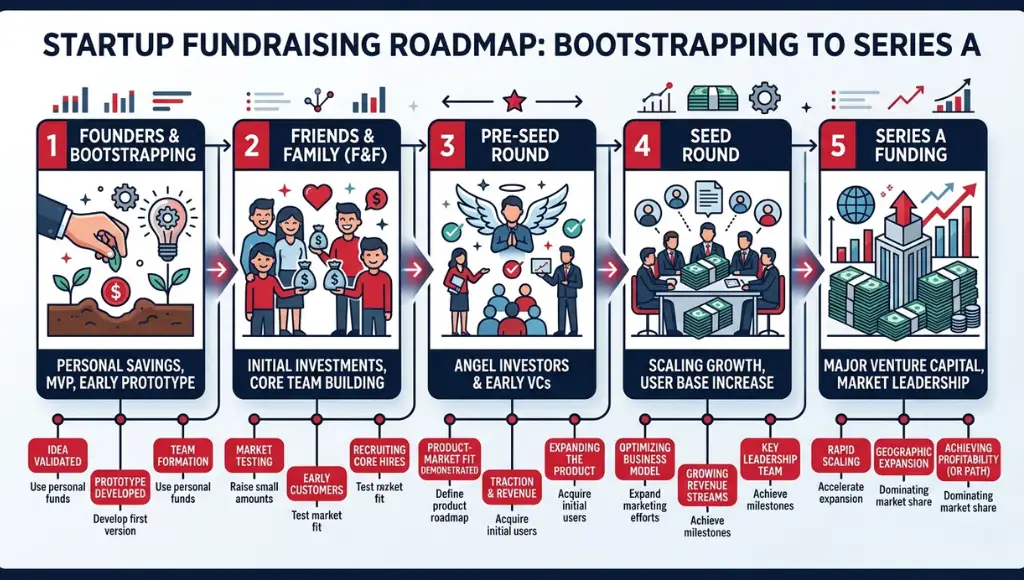

5-Stage Booted Fundraising Framework (Step-by-Step)

The most effective startup booted fundraising strategy follows a sequenced, milestone-driven process. Below is the framework we use with founders at ZPro Studio, built from watching dozens of early raises succeed and fail in real time.

1. Bootstrap to First Revenue (Months 1–4)

Before you think about pitch decks, prove someone will pay you. Your target is $1,000 to $5,000 in monthly recurring revenue using personal savings, pre-sales, or a consulting bridge. This stage answers the most important investor question: does the problem exist, and will people pay to solve it? When I worked with a B2B SaaS founder in 2024, she generated her first $3,200 MRR through five hand-closed deals before spending a single dollar on marketing. That number became the opening line of her seed deck.

2. Validate Unit Economics (Months 3–6)

Bootstrapped startup fundraising without unit economics data is fundraising blind. Calculate your Customer Acquisition Cost (CAC), Lifetime Value (LTV), and payback period. For lean startup capital strategy purposes, you need LTV:CAC above 3:1 before investor conversations begin. Use free-tier tools like Google Analytics and Stripe revenue dashboards to build this picture cheaply. The research is consistent here: investors value a $5K MRR business with a 4:1 LTV:CAC more than a $15K MRR business with no visibility into unit economics.

3. Build the Fundraising Narrative (Months 5–7)

Now translate your traction into a story. A strong bootstrap-to-fundraising roadmap narrative covers three arcs: the problem (with market size data), the proof (your revenue and retention metrics), and the potential (what capital unlocks specifically). Avoid generic TAM/SAM/SOM slides. Investors in 2026 respond to founders who can point to a specific inflection point and say: “With $500K, we triple our outbound capacity and hit $30K MRR by Q3.” Specificity signals execution, not optimism.

4. Selective Investor Outreach (Months 6–9)

Startup funding without venture capital as your only path means knowing your investor landscape. Angel networks, revenue-based financing platforms like Pipe or Clearco, SBIR grants, and micro-VCs under $25M AUM are all valid first-round sources. Target 30 to 40 investors rather than blasting 200. Warm introductions convert 5x better than cold outreach, per SBA investment data. Build your list through accelerators, LinkedIn second-degree connections, and founder Slack communities.

5. Close and Deploy Strategically (Months 8–12)

Once you have term sheets, do not rush to sign the first offer. Use competing interest to negotiate valuation, pro-rata rights, and board composition. After closing, create a tight 90-day deployment plan with three public milestones: one product, one revenue, one team. Public accountability builds investor confidence and sets the stage for your Series A narrative. A client of mine at ZPro Studio followed this exact step in late 2024 and closed a $1.2M pre-seed at a $7M cap, 30% above their original target, purely because they had a competing term sheet in hand.

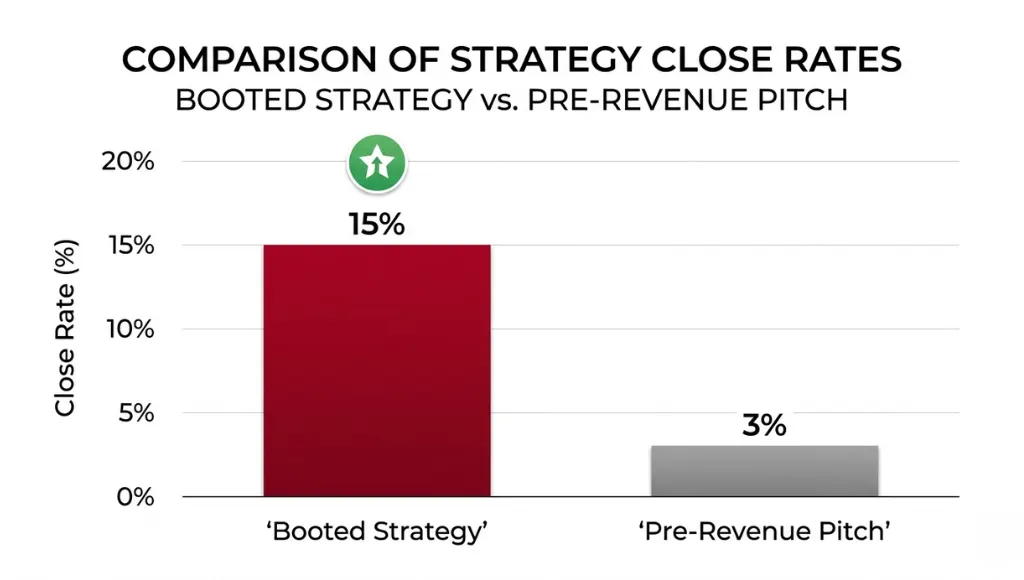

Bootstrapped vs. VC-First vs. Booted Strategy: How They Compare

Most founders treat bootstrapping and fundraising as opposing philosophies. The startup booted fundraising strategy reframes them as sequential phases. Here is how the three main paths compare across the metrics that actually matter.

| Factor | Pure Bootstrap | VC-First (Pre-Revenue) | Booted Fundraising Strategy |

|---|---|---|---|

| Equity Given Up (Seed) | 0% (none raised) | 20–30% | 8–15% |

| Speed to Market | Slower (capital-constrained) | Faster (if you close) | Moderate (structured) |

| Investor Leverage | None needed | Low (investor-led terms) | High (founder-led terms) |

| Close Rate | N/A | 2–4% of pitches | 12–18% of pitches |

| Founder Stress (1–10) | 7 (resource stress) | 9 (rejection + runway) | 5 (milestone-driven) |

| Best For | Lifestyle / niche SaaS | Deep tech, hardware | B2B SaaS, consumer apps |

| Time to Seed Close | N/A | 6–18 months | 9–14 months (with traction) |

| Post-Round Valuation Premium | N/A | Low | High (traction-backed) |

Use a VC-first approach when your business requires significant capital before any revenue is possible (deep tech hardware, biotech, infrastructure). Use a pure bootstrap strategy when you are building a lifestyle business or niche tool with no Series A ambition. Use the startup booted fundraising strategy when you are building a scalable B2B or consumer company and want to raise capital without sacrificing disproportionate equity.

Most experts recommend pitching before you have traction to “get feedback from investors.” In practice, I have found that early pitches mostly produce rejections that damage founder confidence rather than actionable product insights. Save investor meetings for when you have something to show.

Real-World Results: What Happens When Founders Use This Strategy

One of our ZPro Studio clients, a three-person SaaS team building a procurement tool for mid-market retail, applied this self-funded startup growth strategy in 2025. They started with $18K of personal savings, closed their first five customers through direct LinkedIn outreach, and hit $7,200 MRR before contacting a single investor. When they finally entered fundraising conversations, they closed a $750K angel round in 11 weeks at a $5.5M pre-money valuation. Comparable pre-revenue companies in the same cohort were either struggling to raise or accepting convertible notes with punishing caps.

The secondary benefits of this approach are worth naming explicitly. First, you develop genuine product intuition: bootstrapped founders are forced to talk to customers constantly, which shapes a better product than one built in isolation with investor funding. Second, you build a culture of capital efficiency that compounds over time. Third, your cap table stays clean for the investors who matter most at Series A and beyond.

This strategy works best for founders with an identifiable target customer, a repeatable sales motion, and at least one person on the team who can close deals without a full product in place. It will not work for everyone, especially for companies in regulated industries where compliance costs require capital before any sales are possible.

5 Mistakes That Kill a Booted Fundraising Strategy Before It Starts

Raising too early under the guise of "market validation."

Pitching investors to “validate your idea” is rarely a real strategy. Investors are not product advisors. Genuine validation comes from paying customers, not polite feedback from a VC associate.

Bootstrapping indefinitely out of fear.

The bootstrap-to-fundraising roadmap has an endpoint. Some founders get comfortable at $8K MRR and avoid the discomfort of fundraising entirely. If your market has a winner-take-most dynamic, staying capital-light too long is a competitive risk. (I made this mistake myself with an early project, and a well-funded competitor scaled past us in nine months.)

Confusing revenue with investable traction.

Revenue alone is not enough. Investors want revenue plus growth rate plus retention. A business doing $10K MRR but losing 20% of customers monthly is not investable. Fix retention before you raise.

Targeting the wrong investor type at the wrong stage.

A $500K bootstrapped SaaS company should not be pitching Tier 1 VCs with $500M funds. Fit your investor tier to your stage. Micro-VCs, angels, and syndicates are the right audience for a lean startup capital strategy at the seed level.

Neglecting the legal and financial hygiene needed to raise.

Clean incorporation documents, no personal-to-business fund mixing, and a proper cap table management tool (Carta is the standard) are non-negotiable before you accept a term sheet. Messy financials add weeks to due diligence and can kill deals at the finish line.

Frequently Asked Questions About Startup Booted Fundraising Strategy

A startup booted fundraising strategy is a capital-raising approach where founders first self-fund operations to achieve proof-of-concept, then leverage that traction to attract investors on far better terms. It works by sequencing bootstrapping before investor outreach, which improves close rates, protects founder equity, and produces stronger valuations. The core principle: earn the right to raise by proving the business works without outside capital first.

Most founders who follow a disciplined startup booted fundraising strategy reach seed-round readiness in 12 to 18 months, provided they hit key traction milestones such as $5K to $15K MRR or 1,000 active users. The actual fundraising process typically takes an additional 8 to 14 weeks from first outreach to close. Founders with warm investor introductions close significantly faster than those relying on cold outreach alone.

Yes, with some adjustments. Bootstrapped startup fundraising does not require large personal reserves. Many founders start by pre-selling their product before building it, taking on a part-time consulting contract to fund early development, or applying for non-dilutive government grants such as SBIR or state small business programs. The goal is to reduce your cash burn to near zero while proving the product concept with real paying customers.

For B2B SaaS, investors in 2026 prioritize MRR growth rate (ideally 15% month-over-month), net revenue retention above 100%, and CAC payback under 12 months. For consumer apps, they focus on daily active user ratios and 30-day retention. Generic revenue numbers without growth context rarely move seed investors in the current market. Your lean startup capital strategy should be built around generating and documenting these specific metrics.

Absolutely. Startup funding without venture capital is the norm, not the exception: according to the SBA, fewer than 1% of US companies ever receive VC funding. Revenue-based financing, angel rounds, SAFE notes from micro-investors, and cashflow reinvestment are all proven paths to building substantial businesses. The startup booted fundraising strategy is compatible with eventually raising a VC round, but it never makes that round mandatory.

The clearest signal is hitting a growth ceiling that capital would specifically remove. If you have consistent month-over-month growth, a proven sales motion, and a specific deployment plan for capital (hiring, paid acquisition, product development), it is time to raise. If you are still discovering what your customers want, or if your retention is below 60% at 30 days for consumer, keep bootstrapping. More capital does not fix a product-market fit problem.

For most founders following a bootstrap-to-fundraising roadmap, the best first investors are sector-specific angels with operator experience. They move faster than institutional VCs, require less paperwork, and often provide introductions to your second round. Look for angels who have built a company in your category: their network and pattern recognition add far more value than a generic check from a financial-only investor.

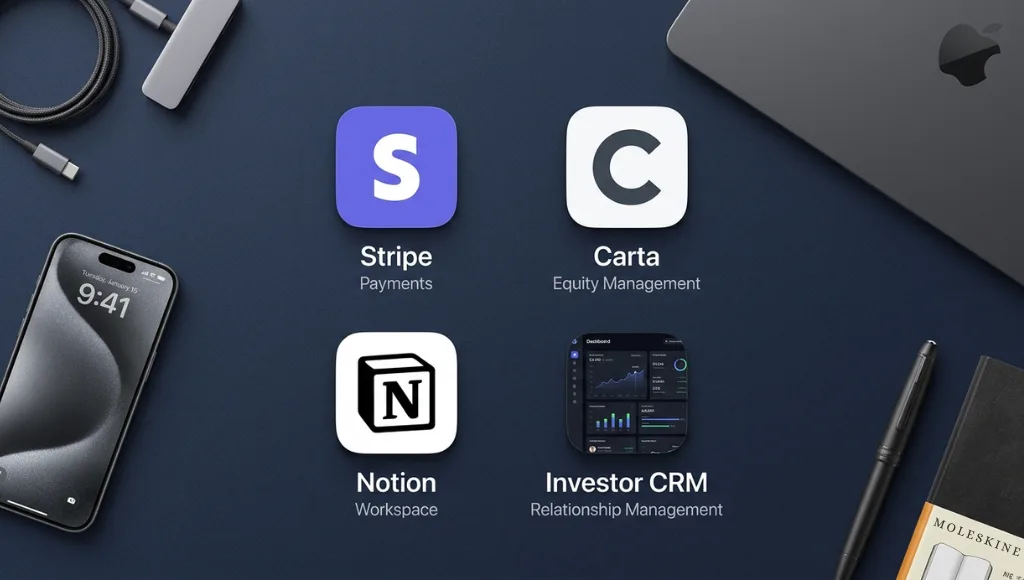

Essential Tools for Your Booted Fundraising Journey in 2026

Executing a self-funded startup growth plan without the right infrastructure wastes time and creates gaps in your data story. Here are the tools I recommend across three categories, based on what actually gets used by our ZPro Studio cohort founders in 2026.

Financial tracking: Stripe for revenue, Baremetrics or ChartMogul for MRR dashboards, and Wave Accounting for early-stage bookkeeping. These three tools together give you the complete unit economics picture investors want to see, at a combined monthly cost under $100.

Cap table and legal: Carta for cap table management from day one, Clerky or Stripe Atlas for clean incorporation. Do not use spreadsheets for your cap table. One error at the Series A due diligence stage can delay a close by weeks.

Investor relationship management: Notion or Affinity CRM to track your outreach pipeline, follow-ups, and investor notes. Treat your fundraising process like a sales process, because it is one. According to Y Combinator’s Seed Fundraising Guide, founders who maintain a structured investor CRM close rounds 30% faster than those managing outreach informally.

Final Thoughts: Play the Long Game and Raise from Strength

After working with dozens of early-stage founders, the pattern is consistent: the startup booted fundraising strategy is not a compromise between building a real business and raising capital. It is the most direct path to doing both well. Here are three things worth committing to memory before you start.

First: traction is your best negotiating tool. Every dollar of revenue you generate before fundraising is worth two dollars of valuation protection at the table. Build the number, then make the call.

Second: the bootstrapped startup fundraising phase is not just about surviving without investment. It is about learning everything about your customer, your cost structure, and your competitive moat before you are accountable to outside capital.

Third: the investors worth working with already respect the lean startup capital strategy. If an investor dismisses your bootstrapped traction and wants to fund your deck instead of your data, that tells you something important about how they will behave on your board.